Something funny is happening with the

price of crude oil. Supply is increasing, demand is decreasing, storage

capacity is running out, and yet the price is going up. Up from $32.84

a barrel on February 26 to $36.33 a week later on March 4. That's a

rise of 10.63% in one week. Up almost another 5% today. If you are

interested in this topic,

listen to about 10

minutes of this Macro Voices

podcast starting about 41 minutes. Then come back and read on. If you

have the time, the entire podcast is worth a listen as are the other

offerings on their website. It seems that speculators anticipating a

rising price have been able to drive the price up based on their will to

see it rise. And foreign oil ministers have cooperated with press

releases hinting at impending production cuts or freezes. The key to

the potential collapse of this house of cards may be the rapidly

approaching limit on crude oil storage capacity.

For background, let's review some basics of crude oil storage in the US (Crude Inventories and Storage Capacities)

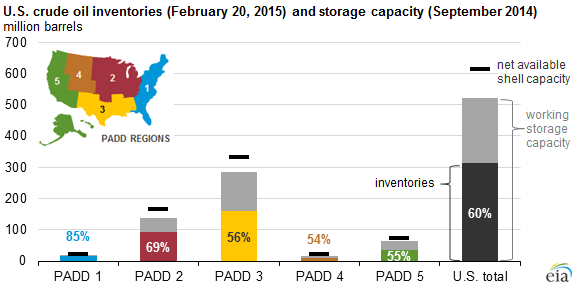

PADD is an acronym for Petroleum Administration for Defense District. The country is divided into PADD districts labeled 1-5. The map above shows the boundaries of the various PADDs and the graph shows the capacity of each. As I mentioned, that data too is a bit dated, but close.

The narrative on the webpage defines the terminology such as the difference between working capacity and shell capacity, so check out the actual page to read that and get a fuller understanding. This diagram below is down at the bottom of the page, and it clarifies the terminology even better.

For current stats on capacity, check this webpage.

As of this writing, November 2015 is the most recently published data

on capacity. March 2016 data will be published at the end of May.

Here are the current stats on available storage courtesy of the US government Energy Information Administration.

Current working capacity is just over 500 million barrels. Shell capacity about 100 million barrels more. That extra 100 million barrels is referred to as contingency space, so I'm not sure when or even if that ever comes into play. And BTW, these capacities are separate from what's known as the Strategic Petroleum Reserve. That capacity is a further 700 million barrels or so and it it practically maxed out now.

Here are the current stats on available storage courtesy of the US government Energy Information Administration.

Current working capacity is just over 500 million barrels. Shell capacity about 100 million barrels more. That extra 100 million barrels is referred to as contingency space, so I'm not sure when or even if that ever comes into play. And BTW, these capacities are separate from what's known as the Strategic Petroleum Reserve. That capacity is a further 700 million barrels or so and it it practically maxed out now.

The

following 2 charts are representations of current stocks of crude oil

relative to overall capacity, and they are more current than the chart at the top of the page. The first chart is stocks vs capacity for only

PADD 3 (Gulf Coast) and Cushing, Oklahoma (part of PADD 2). Cushing is listed

separately because it is important to oil markets as the point of delivery for the WTI futures

contract for crude. WTI futures contracts for delivery at Cushing are what determines the price of crude. Cushing and PADD 3 together

make up almost 70% of US commercial storage. Notice we are currently at

84% capacity for these sites, and Cushing alone is at 89%.

Finally, here is an excerpt from the most recent EIA weekly report on crude stocks as of this writing.

(Click here for most recent report)

The third line is the Strategic Petroleum Reserve which is at capacity, not changing and thus irrelevant. The relevant line is line 2: Commercial (Excluding SPR). The value is 518 million barrels which is a 10.4 million barrel build (2%) from the previous week.

(Click here for most recent report)

The third line is the Strategic Petroleum Reserve which is at capacity, not changing and thus irrelevant. The relevant line is line 2: Commercial (Excluding SPR). The value is 518 million barrels which is a 10.4 million barrel build (2%) from the previous week.

Summary:

All time high in crude in storage. Still increasing at significant

rate. Rapidly approaching full capacity. Now is when the 10 minute

part of the podcast comes into play. Price will only loosely obey

supply/demand rules as long as storage is adequate. Speculation and

rumors of production cuts/freezes can have significant influence. But

when storage runs out, price can plummet as that represents suddenly

reduced demand.(N0 0ne demands crude if they're not using it and now

they can't even store it).

So why in the face of this did oil go up 10% last week alone and a further 5.7% today?

Jess